Understanding the Mortgage Process for Lenders

The mortgage process is a critical pathway for lenders, as it encapsulates the various stages that a borrower goes through to secure financing for a property. By comprehending the mortgage process for lenders, financial institutions can enhance their efficiency, improve customer satisfaction, and maintain competitive positioning in the market. This guide delves into the key stages, common challenges, and best practices that lenders should be aware of throughout the mortgage process.

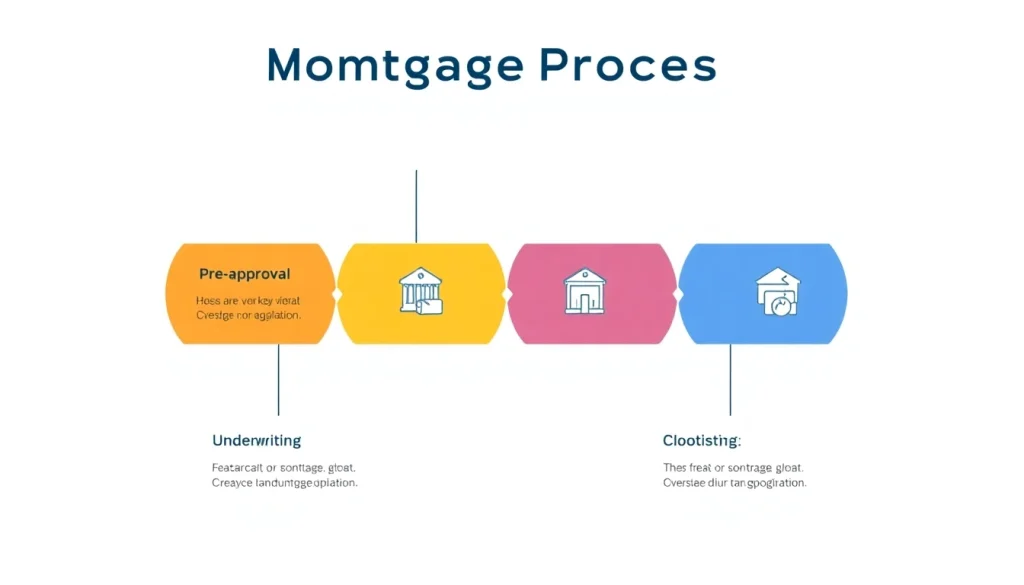

Key Stages in the Mortgage Process

The mortgage process can be broken down into several key stages, including pre-approval, house shopping, mortgage application, loan processing, underwriting, and closing. Understanding these stages helps lenders provide better guidance to borrowers and streamline their workflows.

- Pre-approval: During this initial stage, lenders assess a borrower’s financial status to determine their eligibility for a loan. This helps potential homeowners understand their budget when searching for property.

- House Shopping: Once pre-approved, borrowers can confidently shop for homes within their price range, which helps set realistic expectations.

- Mortgage Application: After selecting a property, borrowers submit a mortgage application along with necessary documentation to the lender.

- Loan Processing: Lenders process the loan application by verifying the applicant’s information, analyzing credit history, and ensuring all necessary documents are collected.

- Underwriting: This critical phase assesses the risk associated with the loan. Underwriters examine the borrower’s financial profile and the property in detail.

- Closing: Finally, all parties involved meet to sign documents, finalize the loan, and complete the transfer of the property.

Common Challenges Faced by Lenders

Lenders often encounter challenges that can impact the mortgage process. Some of the most common issues include:

- Delays in Documentation: Borrowers may not provide all required documentation in a timely manner, leading to processing delays.

- Changing Regulations: Keeping up with frequent changes in mortgage regulations and compliance can hinder the process.

- Market Fluctuations: Economic shifts can affect interest rates and housing prices, causing uncertainty for both lenders and borrowers.

- Technology Integration: Adopting new technologies for processing loans can be resource-intensive and requires proper training for staff.

Importance of Transparent Communication

Effective communication between lenders and borrowers can significantly reduce misunderstandings and errors during the mortgage process. Lenders should prioritize:

- Regular updates on the application status and timelines.

- Clear explanations of the documents required throughout the process.

- Open channels for borrowers to ask questions or voice concerns.

Step-by-Step Breakdown of the Mortgage Process

Initial Steps: Pre-Approval and Documentation

The first step in the mortgage process begins long before the actual property search: the pre-approval. A pre-approval provides a strong estimate of the amount of money a lender is willing to loan based on the borrower’s financial condition. This section highlights necessary documentation:

- Proof of income (such as pay stubs and tax returns)

- Credit reports

- Employment verification

- Debt details (credit cards, student loans, etc.)

- Identification and Social Security number

Lenders should ensure they obtain comprehensive information from borrowers to avoid bottlenecks later in the process.

Applying for a Mortgage: What Lenders Need

Once borrowers find a property they wish to purchase, they proceed to formally apply for a mortgage. This stage involves:

- Completing a detailed mortgage application, which includes personal details and loan amount.

- Submitting all supporting documents to the lender.

- Discussing potential loan products and terms with the lender, ensuring that the borrower understands their options.

At this stage, lenders also assess the type of mortgage that best suits the borrower’s needs (fixed-rate vs. adjustable-rate mortgages, for example).

Understanding Underwriting Basics

Underwriting is arguably one of the most significant stages in the mortgage process. During this phase, underwriters verify the borrower’s creditworthiness and assess the property’s value:

- Creditworthiness: Analyzing the borrower’s credit history, debt-to-income ratio, and overall financial profile helps determine whether the lender should approve the loan.

- Property Assessment: An appraisal ensures the property value meets or exceeds the loan amount, protecting the lender’s investment.

Underwriting can identify red flags early, allowing for necessary adjustments before the closing process.

Best Practices for Lenders in the Mortgage Process

Improving Efficiency Through Technology

Modern technology has revolutionized the mortgage process. By utilizing software solutions for loan processing, lenders can significantly enhance efficiency and communication:

- Automated Document Collection: Using technology to collect and verify documents reduces the manual workload on staff.

- Real-Time Communication Tools: Platforms that facilitate immediate updates for borrowers regarding their loan status can improve customer experience.

Investing in technology not only speeds up the process but also allows lenders to take on more clients.

Maintaining Compliance and Regulations

Compliance is paramount in the mortgage industry. Lenders should regularly review and adapt their processes to abide by evolving regulations:

- Establish a compliance team dedicated to monitoring regulatory changes.

- Utilize compliance software that helps automate compliance checks and reporting.

- Engage in ongoing training for staff to remain knowledgeable about current laws and regulations.

Building Relationships with Clients

Fostering strong relationships with clients can lead to increased loyalty and repeat business:

- Offer personalized service and regular check-ins to discuss any concerns.

- Educate clients on the mortgage process to empower them and alleviate anxiety.

- Solicit feedback to improve service offerings and client experiences.

Metrics for Success in the Mortgage Process

Key Performance Indicators for Lenders

To gauge success within the mortgage process, lenders should monitor relevant Key Performance Indicators (KPIs), such as:

- Loan origination volume

- Approval rate (percentage of applications approved)

- Average processing time (from application to closing)

Customer Satisfaction and Retention Rates

Beyond quantitative metrics, understanding customer satisfaction and retention is crucial. Lenders can utilize:

- Customer satisfaction surveys to gather feedback

- Net Promoter Score (NPS) to assess brand loyalty

Following up with clients post-closing can lead to valuable insights and repeat business.

Analyzing Loan Processing Times

Evaluating and reducing loan processing times can improve overall efficiency:

- Track processing times at each stage (application, underwriting, closing).

- Identify bottlenecks and areas for improvement, whether in documentation, communication, or technology.

Future Trends in the Mortgage Process for Lenders

Technological Innovations on the Horizon

The landscape of mortgage lending is continuously evolving, driven primarily by technological advancements:

- AI and Machine Learning: Increasingly utilized for risk assessment and personalized lending criteria.

- Blockchain Technology: Potential for enhancing the security and transparency of transactions.

Impact of Market Changes on Lending Practices

Market fluctuations can significantly influence lending practices:

- Lenders must remain adaptable to shifts in interest rates, property values, and borrower financial health.

- New regulations and market conditions necessitate ongoing training and adaptability among lending teams.

Preparing for Evolving Consumer Expectations

As consumers become more informed and tech-savvy, lenders must adjust to meet their expectations:

- Offer seamless digital experiences alongside personalized service.

- Provide access to educational resources about the mortgage process.